Welcome to the British Association of Former United Nations Civil Servants (BAFUNCS)

Article Categories

Select a category below to filter those articles

- All

- Executive Committee

- Kent & Sussex

- London

- Members' Home Page

- Public Home Page

- UNCRP

We are pleased to inform you that Supplement no. 3 (2021-2025) to the Guide for Researchers to the UN Career Records Project (UNCRP) is now available and posted on the website . This was completed by Bill Jackson as his final contribution to UNCRP and, as usual, he has done an excellent job. UNCRP Supplement no. 3 (2021-2025) This third Supplement to the Guide updates the summaries of careers and contributions to the UNCRP. The material is intended to be of use to researchers interested in international cooperation and global governance. It contains additional information related to existing entries in the Guide and Supplements 1 and 2; new material received from contributors since the original Guide and Supplements were published; and an Index of Keywords contained in this Supplement. New contributors covering many different aspects of the work of the United |Nations System include Nicola Dahrendorf, Phyllis Camilla Ruegg, Margaret Branch, Alan Everest, Caroline Jones, Omar Noman, Colin Fraser, and Patricia Joan Marlowe. There are also additional contributions from, amongst others, Peter Marshall, Richard Jolly, Terence Jones, Bill Jackson, and Patrice-Ariel Français. Terry and I would be delighted to provide support to anyone considering adding further materials to the steadily growing archive. Any material can be considered if not already formally published, either in hard copy or electronic form. It is also important to know that you can place a time embargo of your choosing on material which you may regard as sensitive. We can also arrange to record interviews if this is your preferred medium. Regarding digital material, while it is being preserved, the systems are not in place to make it available securely through terminals in the reading rooms. However, there has been important progress recently with the Bodleian Library authorised to acquire a Digital Asset Management System (DAMS), which will provide access to digital material that cannot be made openly available online, through a controlled access, “virtual reading room” environment. Procurement is expected in 2026 and the first phase of cataloguing the backlog of digital material expected to start in 2027. Nicholas Rosellini & Terence Jones Contact the UNCRP Team

Kent and Sussex Region held their summer lunch at the Alfriston Hotel, Alfriston, East Sussex on 2nd July. Alfriston is a charming Sussex village between Lewes and Eastbourne within the South Downs National Park. The Alfriston Hotel has recently undergone a major renovation and was very comfortable, with a first class kitchen – good food and conversation was much enjoyed by us all. L to R: Joan Wilson, Peter Sanders, Richard Sydenham, Sheila Cooper, Mike Askwith, Heather Johnson, Anna Eliatamby, Elsbeth Hinser. Thanks to Mike Askwith for his drawing of Alfriston Hotel. Our next get-together will be at Chichester on Thursday, 10 September which will include a guided tour of Chichester Cathedral followed by lunch. All members and guests from other regions are welcome to attend. More details to follow closer to the date. Heather, Terri and Richard

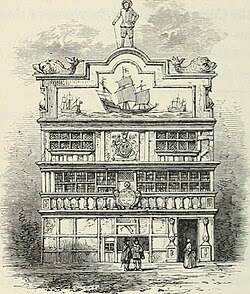

Popular and selling out fast! We are delighted to be able to invite you to a guided walking tour that explores the fascinating and often complex story of the East India Company and its history in the City of London. The East India Company was founded in 1600 and went on to become one of the most powerful commercial organisations in history, shaping global trade, politics, and empire. From spices and textiles to tea and territory, its legacy is written into the streets of the City of London. This walk brings those stories to life in the very places where decisions were taken, fortunes were made, and Britain’s imperial story was directed. The tour will be guided by Lisa Honan CBE, former diplomat, who spent her career in international development. One of her roles was as Governor of St. Helena, Ascension and Tristan da Cunha. St. Helena itself was ruled by the East India Company for over 200 years, making it a unique and personal link to the Company’s history. Lisa is also a City of London guide and brings together historical scholarship, lived experience, and engaging storytelling. If interested please contact Shahnaz Lockwood at shaanaah@aol.com Joining Instructions: Starting point: Monument Underground Station, Fish Street Hill exit. Time : 2pm Finishing point: The Royal Exchange. Duration: approximately 2 hours 15 minutes The walk is designed to be accessible and enjoyable: Pace: slow and steady Terrain: no hills Cost: £20pp (cash) – payable on the day* It is a thoughtful, informative and atmospheric walk that reveals how the City of London was the engine room of an organisation that shaped the modern world. Lisa’s website is here https://www.walkinglondontours.co.uk/ *Please note that if you reserve, it is a commitment to pay £20. Spaces are filling fast and are limited to 25 people.